As the October 2025 deadline approaches, the widespread implementation of Beneficiary Verification (VoP) across the SEPA area marks a turning point in payment security. For major Finance and Treasury departments, as well as finance IT managers, this initiative is no longer just a compliance project, it now lies at the heart of operational resilience, transaction integrity, and data governance challenges.

A Structural Response to Payment Fraud

VoP (Verification of Payee) aims to confirm, via a PSP or bank, the match between a beneficiary’s name and their IBAN before executing a transfer. This process blocks attempted identity theft or manipulation of banking details at the source such as CEO fraud or fake supplier scams. For European treasurers, VoP has become a real safeguard, protecting not only against financial losses but also damage to corporate reputation.

VoP Response Statuses: Critical Indicators for Payment Management

The effectiveness of VoP relies on standardized response statuses defined by the European Payments Council (see specifications), which must be properly integrated into ERP and TMS workflows. Each status determines the next step in the payment process:

Match (exact match): The beneficiary’s name and IBAN match perfectly.

→ Payment is automatically approved.Close Match (partial match): There is a discrepancy (e.g., trade name, legal name variation), with severity rules to be defined before implementing VoP in the system.

→ The process might trigger manual verification or supplier contact.No Match: A significant difference between the entered data and the bank’s records.

→ Payment is blocked. An investigation is launched to clarify the issue.Unavailable / Technical Error: The verification service is unavailable.

→ Payment is suspended and routed through an exception process.

Proper orchestration of these scenarios within your systems is critical to avoid unnecessary blocks, security breaches, and payment delays that can disrupt your entire Treasury operation.

Can VoP Be Integrated Into Your Systems Today?

Implementing a VoP service doesn’t solely depend on banking network readiness. It must also be anticipated within existing systems—such as ERPs and TMS—by checking with your software vendor whether it can connect to a VoP service and integrate it into workflows.

While not all banks are yet ready to offer VoP (despite being required to do so from October 2025), services like SEPA Diamond and fraud prevention software providers already offer APIs for integrating Verification of Payee into your TMS, ERP, payment factory, or bank communication software.

Testing environments are available to simulate VoP scenarios, validate business rules, and train your teams.

VoP in Datalog TMS

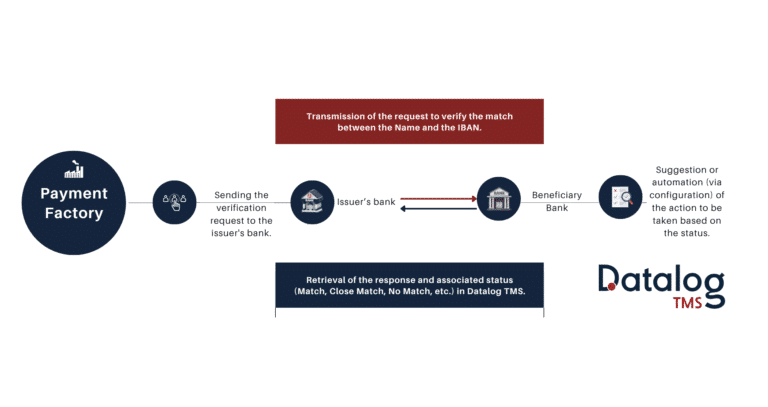

For example, the VoP module integrated into the Payment Factory of Datalog TMS supports all stages of beneficiary verification:

Sending a verification request to the sender’s bank, which then queries the beneficiary’s bank

Receiving and displaying the response and status (Match, Close Match, No Match…) in Datalog TMS

Recommending or automating next steps based on configuration and status

Data Governance and Change Management

Mapping data sources (ERP, CRM, Excel files, etc.) Cleaning up IBANs and associated names Clearly defining business and IT responsibilities Raising awareness among accounting, procurement, and treasury teams about types of fraud Implementing VoP requires a deep review of vendor data quality and validation processes. This includes: Mapping data sources (ERP, CRM, Excel files, etc.) Cleaning up IBANs and associated names Clearly defining business and IT responsibilities Raising awareness among accounting, procurement, and treasury teams about types of fraud

October 2025: An Ambitious but Realistic Deadline?

While the European Commission is pushing for the widespread adoption of VoP by October 2025 for intra-EU transfers, banks’ levels of preparedness remain uneven. Interoperability challenges, format standardization, and legal harmonization between Member States all make smooth implementation more complex.

In this context, companies must take the lead: rather than waiting for full banking standardization to secure their payment flows, they should rely on autonomous and adaptable solutions onto which VoP can add an extra layer of security.

In Conclusion

More than just a technical check, VoP is a payment security tool for Treasury departments. It prompts a broader reflection on how payment flows are secured and further professionalizes supplier relationships, much like KYC has done on the client side. By aligning with digital transformation priorities and compliance requirements, VoP becomes a strategic investment for companies, serving their operational performance and resilience.