The terms “Payment Hub” and “Payment Factory” are frequently used interchangeably; however, there are significant distinctions between the two. Here is an overview:

Payment Hub

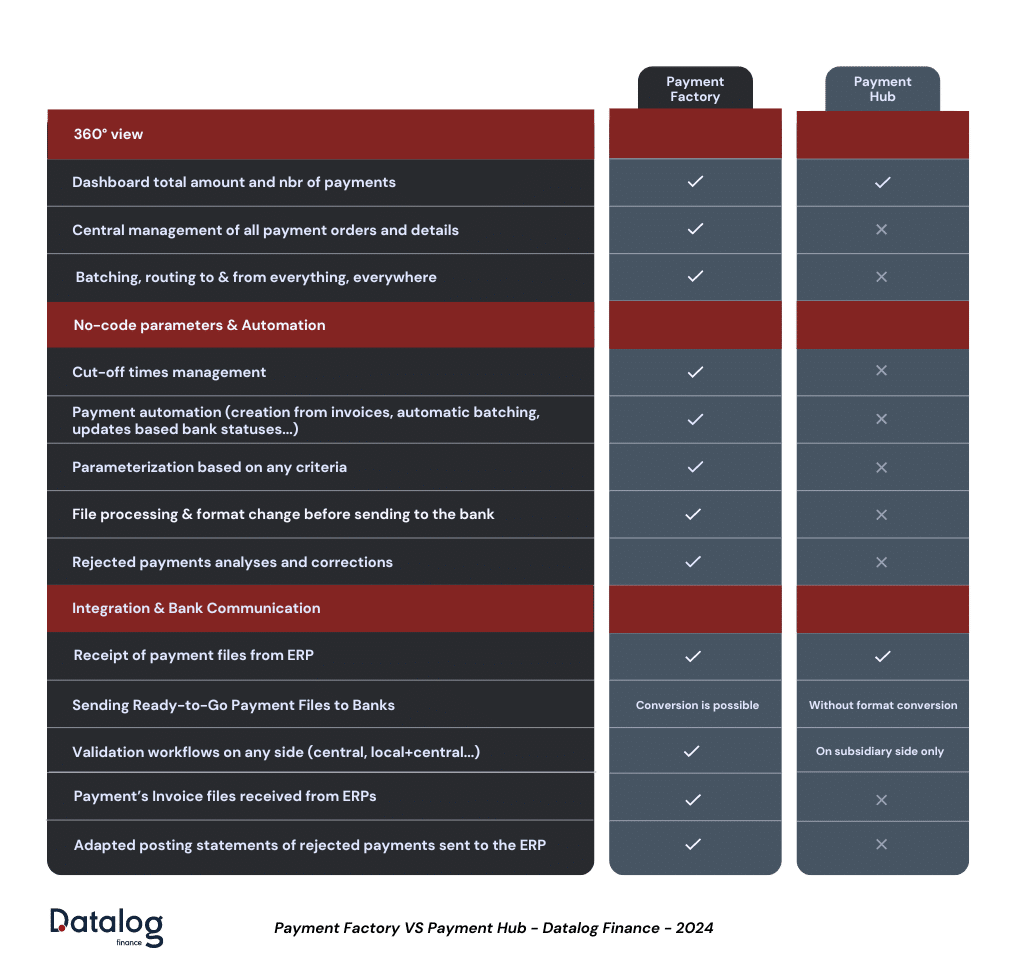

A Payment Hub offers a simple solution for centralizing payment processes. It achieves this by executing payments based on pre-defined rules within a strict, non-customizable workflow. All subsidiaries can connect to this centralized system for sending their payments directly to various banks.

This solution is particularly well-suited for:

- Mid-sized to intermediate-sized organizations

- Companies with limited needs for:

- Centralization and standardization of payment processes

- International acquisitions management

- Customization of workflows, batching criteria, task scheduling, etc.

Functionalities

- Receives payment files from ERPs.

- Implements validation workflows on the subsidiary side.

- Sends validated payment files to banks.

- Crucially, it doesn’t modify the file format received from the ERP.

- The hub simply validates and transmits the data “as is” to the bank.

- Monitors payment files in a global dashboard.

- It can show totals and counts

- It may not display individual payment details.

Payment Factory

A Payment Factory is a comprehensive and customizable payments solution designed to address both basic and complex payment needs of large enterprises. It also enables adaptation to current and future processes (file formats, workflows, etc.).

Unlike a Payment Hub, a Payment Factory can create payments from multiple sources (e.g., invoices in the ERP), convert various payment file formats from different entities, and consolidate them to target banks for each centralization point (e.g., by region).

In fact, Payment and collection processes are standardized, regardless of the sending or beneficiary country which results in enhanced bank relationship management. By streamlining their banking relationships, companies are better positioned to negotiate more favorable bank fees due to the consolidation of a larger volume of transactions per banking partner.

Functionalities (Includes Payment Hub functionalities)

- Receives payment files (payments and/or invoices) from ERPs.

- Imports all orders into a database for central management.

- Creates new payments from invoices based on user-defined rules. (This goes beyond simply processing existing payment files)

- Offers advanced controls for payment orders using internal rules and external AML/CFT checks.

- Implements any kind of workflow: central, local, local+central, blackbox…

- Enriches payment data with information from other systems.

- Manages payment batches (creation, modification) based on user-defined rules.

- Sends validated payment files to banks, potentially adapt the format of payment file received from the ERP.

- Provides a more comprehensive global dashboard that displays details of all payments within a file, in addition to totals and counts.

- Tracks payment statuses by receiving reports from banks and updating individual payment records.

- Analyzes rejected payments to identify and minimize future rejections.

- Integrates with ERPs for sending posting statements of rejected payments in the expected format.

- Optimizes cash flow through features like managing bank cut-off times and organizing group payment campaigns.

Datalog-specific features: Consolidated batch creation and intelligent bank routing based on allocation rules. (These are additional functionalities beyond the core payment processing capabilities)

In essence

A payment hub focuses on streamlined execution of pre-defined payments. It validates and transmits data as received, offering a basic level of automation and control.

A payment factory provides a more comprehensive payment processing environment. It goes beyond execution to encompass creating new payments, advanced controls, data enrichment, and sophisticated workflow management. It offers a higher level of automation, control, and visibility.

Payment Factory vs Payment Hub Comparison

How Datalog TMS Payment Factory Optimizes Payments

Datalog TMS Payment Factory offers several functionalities that streamline and optimize your payments:

Batching and Routing

- Consolidated Batch Creation: Gather payments from any ERP and subsidiary to create new batches based on user-defined rules.

- Grouping Options: Group payments by various criteria like currency, amount range, country, beneficiary bank, etc. This allows for better organization and management of payments.

- Intelligent Bank Routing: Route payments to specific banks based on pre-negotiated allocation percentages. (e.g., X% of payments to Bank 1, Y% to Bank 2, etc.). This ensures efficient distribution of payments based on your banking agreements.

Example: Optimizing Payments with POBO (Payment On Behalf Of)

Datalog TMS Payment Factory empowers you to manage payments on behalf of (POBO) subsidiaries, significantly reducing costs and centralizing control:

Converting Cross-Border Payments to Domestic: By grouping payments by currency and routing them to bank accounts held in the corresponding country, you can convert cross-border payments into domestic transactions to reduce payment fees and centralize FX Management for the group treasury, leading to better control and potentially more favorable exchange rates.

Scenario: A French subsidiary needs to pay an invoice to a Japanese supplier. Traditionally, the ERP would generate a cross-border payment debiting the French subsidiary’s account, incurring high fees and FX risks.

Datalog TMS Payment Factory Solution:

- Gathers all payments from all subsidiaries.

- Groups payments into batches based on currency (e.g., all Japanese Yen payments).

- Each batch is routed to a bank account held by Group Treasury in Japan (assuming they have one).

- Group Treasury handles the payment to the Japanese supplier, effectively converting it to a domestic transaction within Japan.

- This approach minimizes fees for the subsidiary and centralizes FX management for better control.

Datalog TMS Import/Export Module: Seamless Data Exchange

For a Payment Factory to operate efficiently, it needs a robust import/export module that simplifies data exchange with ERPs and banks without requiring programming expertise. This no-code module of Datalog TMS offers several key features:

- Flexible File Format Creation: Create new file formats from scratch to accommodate various data structures used by different ERPs and banks.

- Mapping and Interface Design: Easily map external file fields to corresponding internal database fields, ensuring accurate data transfer.

- Data Transformation: Utilize correspondence tables to convert data during import or export to match the required format.

- Data Enrichment: Enhance payment data by incorporating information from other databases within your system.

Data Validation and Controls: Implement controls to ensure data accuracy for critical fields like amount, bank account details, and SWIFT codes.

Key Benefit: User-Friendly Configuration

All these functionalities within the import/export module can be configured by any user without requiring technical knowledge. This empowers users to manage data exchange processes efficiently, reducing reliance on IT resources.